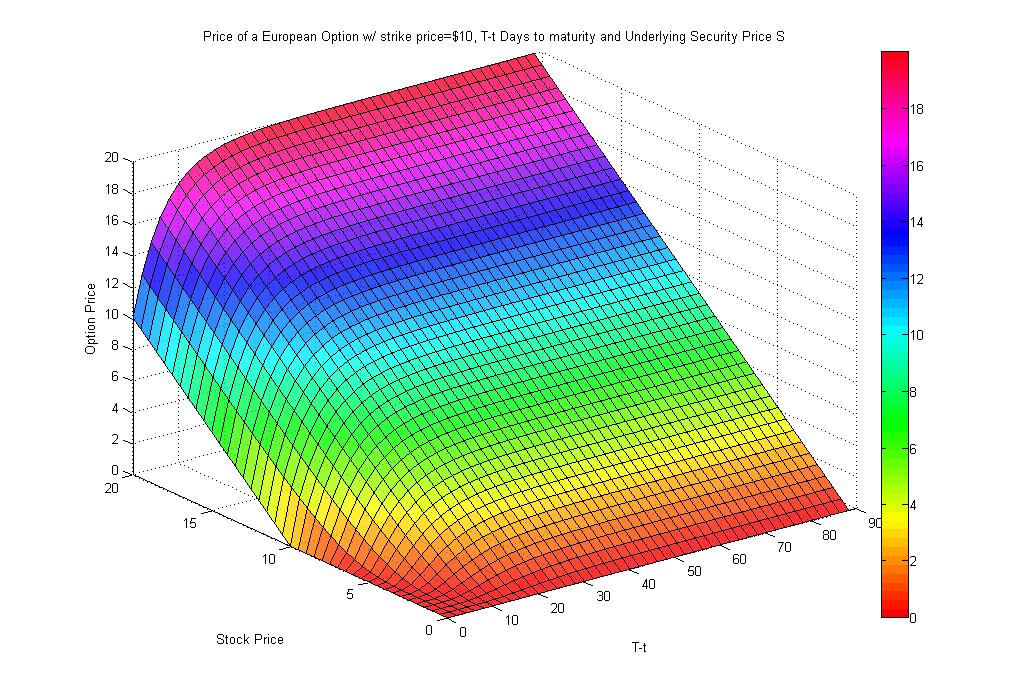

Black Scholes ( Black 76 ) Formula in Endur with Delayed Payment (from Exercise Date)

This document shows the formula used to derive Option Value using Black Scholes ( Black 76 ) formula applied to commodity options

This document shows the formula used to derive Option Value using Black Scholes ( Black 76 ) formula applied to commodity options

A presentation explaining how FX Conversion issues can affect the Delta of Commodity deal , and some possible solutions to this.

Since the addition of formula functions, for example to assess different volume types (e.g. nominated

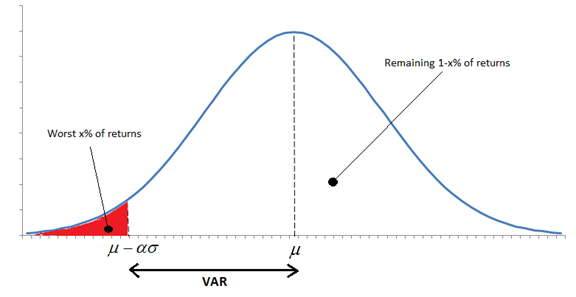

VaR is a measure of the expected loss over a given time horizon at a given confidence interval

A presentation that looks at how Projection Methods in Endur are used to created pricing structures.

Lets say we are a USD reporting company trading EUR denominated Oil products. Oil is quoted in USD so there is a FX risk.