DevOps and ETRM: A Strategic Approach for Driving Value

If you are implementing or upgrading your Energy Trading & Risk Management (ETRM) system, now is the time to integrate

If you are implementing or upgrading your Energy Trading & Risk Management (ETRM) system, now is the time to integrate

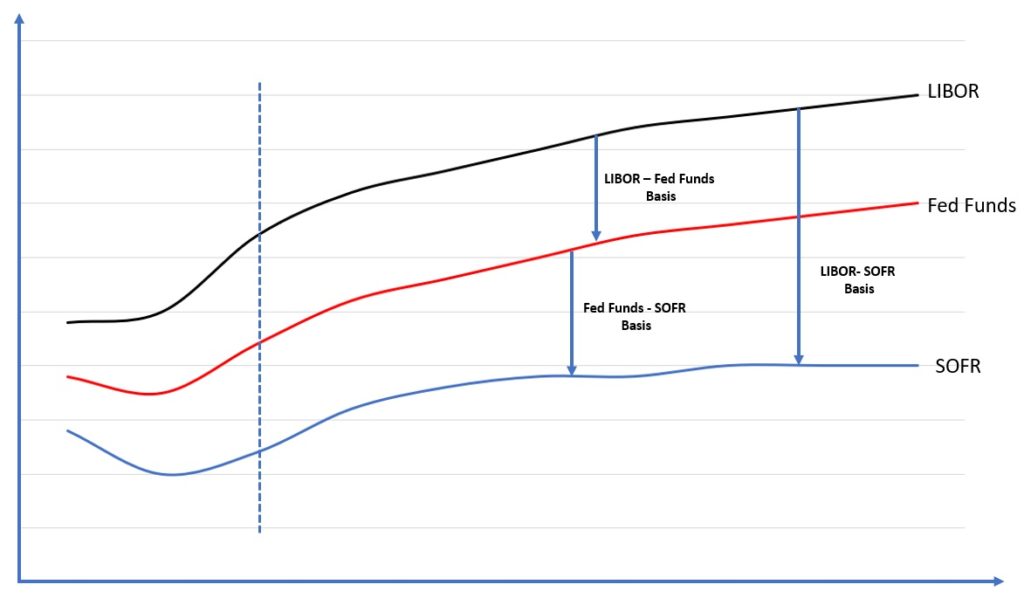

KWA’s Stephen Gillanders insightful article details why and how LIBOR is being replaced and what organisations need to do about the transition from LIBOR to Risk Free Rates in 2021. This has implications for business-critical software like ETRMs, CTRMs and TMS, and is where expert guidance from KWA can help manage the system transition.

The benefits of automation are widely applicable and proven. At the highest level it comes down to one fundamental advantage: efficiency. As companies strive to become more efficient, automation – wherever and whenever possible – is the clear answer.

If you are implementing or upgrading your Energy Trading & Risk Management (ETRM) system, now is the time to integrate

In any organisation, core values serve as guiding principles. At KWA Analytics, our values aren’t just words; they are the

Orchestrade and KWA Analytics, an award-winning, capital and energy market system specialist consulting group, have announced a strategic partnership to

")